What Is an Insurance Actuary?

Understanding the intricacies of the insurance industry can be daunting, but it’s crucial for anyone involved in this field to grasp the roles of key professionals like insurance actuaries. An insurance actuary plays a vital role in assessing risk and ensuring the financial stability of insurance companies. This page aims to demystify the role of an insurance actuary, explore the differences between actuaries and underwriters, and provide a comprehensive overview of what it means to be an actuary. Whether you’re considering a career in this field or simply curious about the profession, this guide will provide you with valuable insights and practical information.

What Is an Insurance Actuary?

Definition and Role

An insurance actuary is a professional who uses mathematical, statistical, and financial theories to study uncertain future events, particularly those of concern to insurance and pension programs. They are pivotal in designing insurance policies, setting premium rates, and ensuring the financial viability of insurance products. Their expertise helps insurance companies understand and manage risks effectively, allowing them to remain profitable while offering fair and competitive premiums.

Skills and Qualifications

To become an insurance actuary, one must possess a strong foundation in mathematics and statistics. Analytical skills are paramount, as actuaries must analyze complex data to make informed decisions. Typically, actuaries have a degree in mathematics, statistics, actuarial science, or a related field. In addition to formal education, actuaries must pass a series of professional exams to gain certification. These exams are rigorous and cover a range of topics, including probability, financial mathematics, and actuarial modeling.

Day-to-Day Duties

An actuary’s daily tasks can vary, but they often include assessing financial risks, creating models to predict future events, and developing strategies to mitigate potential losses. For example, an actuary might analyze data to determine the likelihood of policyholders filing claims and use this information to set appropriate premium rates. They also play a crucial role in ensuring that insurance companies maintain sufficient reserves to pay future claims. A real-life example of an actuary’s impact is seen in natural disaster insurance, where actuaries assess the probability of events like hurricanes or earthquakes and help design policies that balance affordability with financial protection.

Importance in the Industry

Insurance actuaries are indispensable to the industry because they provide the analytical backbone that supports financial decision-making. By accurately assessing risk, actuaries help insurance companies price their products competitively and ensure they can meet future claims. This not only protects the company’s financial health but also safeguards policyholders, ensuring they receive the coverage they need when they need it most.

Actuary vs. Underwriter

| Category | Actuary | Underwriter |

| Role Definition | Analyzes risk and designs insurance policies | Evaluates insurance applications |

| Required Skills | Mathematical, statistical, analytical | Analytical, decision-making, communication |

| Educational Background | Degree in mathematics, statistics, actuarial science | Degree in finance, business, related fields |

| Daily Responsibilities | Risk assessment, premium setting, financial modeling | Application review, risk evaluation, policy issuance |

| Career Outlook | Opportunities in various industries | Specialization within insurance industry |

Definition and Role Comparison

While both actuaries and underwriters work in the insurance industry, their roles are distinct and complementary. An actuary focuses on analyzing data to assess risk and predict future events, using this information to set premium rates and design insurance policies. On the other hand, an underwriter evaluates individual applications for insurance, determining whether to accept or reject them based on the risk they pose.

For instance, when a person applies for health insurance, the underwriter reviews their medical history and other risk factors to decide if they should be granted coverage and at what premium. The actuary, however, would have developed the underlying statistical models and risk assessments that guide the underwriter’s decisions.

Skills and Qualifications

Both professions require strong analytical skills, but the focus differs. Actuaries need a deep understanding of mathematics, statistics, and financial theory, typically holding degrees in these fields and passing a series of professional exams to become certified. Underwriters, while also needing analytical skills, often have backgrounds in finance, business, or related fields and may require different certifications depending on the specific area of insurance.

Responsibilities and Daily Tasks

An actuary’s responsibilities include creating models to predict the likelihood of future events, setting premium rates, and ensuring that insurance companies have adequate reserves. They might work on long-term projects, developing new insurance products or refining existing ones based on emerging data and trends.

Underwriters, in contrast, work more on a case-by-case basis. Their daily tasks involve reviewing insurance applications, assessing risk factors, and making decisions on whether to issue policies. They must balance the need to minimize risk for the insurance company with the goal of offering coverage to as many applicants as possible.

For example, in auto insurance, an actuary might analyze data on accident rates, vehicle safety features, and driver demographics to determine premium rates for different types of drivers. An underwriter would then use this data to evaluate individual applications, deciding if a particular driver should be offered coverage and at what price.

Career Outlook and Opportunities

Both actuaries and underwriters have strong career prospects, but the paths can differ. Actuaries often find opportunities in various industries, including finance, healthcare, and pensions, in addition to insurance. They can advance to senior roles such as chief actuary or move into executive positions within companies.

Underwriters typically progress within the insurance industry, with opportunities to specialize in areas like health, auto, or property insurance. They may advance to senior underwriter positions, manage underwriting teams, or move into broader managerial roles within insurance companies.

What Is an Actuary?

An actuary is a professional who uses mathematics, statistics, and financial theory to analyze and solve problems related to risk and uncertainty. While often associated with the insurance industry, actuaries work in various fields, including finance, healthcare, and pensions, where they assess risks and develop strategies to manage them.

Fields of Work

Actuaries are not limited to the insurance sector. They play critical roles in:

- Finance: Helping financial institutions manage investment risks and develop strategies for financial stability.

- Healthcare: Working with health insurers and providers to develop sustainable healthcare plans and manage costs.

- Pensions: Designing pension plans and ensuring they remain financially viable over the long term.

Skills and Qualifications

Actuaries require a robust set of skills, including advanced mathematical abilities, proficiency in statistics, and strong analytical thinking. Educational qualifications typically include degrees in mathematics, actuarial science, or related fields. Professional certification involves passing a series of rigorous exams covering topics such as probability, financial mathematics, and risk management.

Importance Across Industries

The expertise of actuaries is crucial in various industries. In finance, they help institutions manage investment risks and comply with regulatory requirements. In healthcare, actuaries design insurance plans that balance affordability with comprehensive coverage. In the pension sector, they ensure that retirement plans are sustainable and can meet future obligations.

For example, an actuary working in a pension fund might analyze demographic trends to predict future retiree populations and ensure that the fund has enough resources to pay out benefits. Their work helps ensure financial security for retirees and stability for the pension system.

Real-Life Examples and Case Studies

Insurance Industry

In the insurance industry, the role of an actuary is both critical and multifaceted. When an insurance company needs to develop a new life insurance product, the actuary’s job is to analyze extensive data sets, including life expectancy statistics, health trends, and economic indicators. This analysis helps in determining the likelihood of policyholders making claims. By building sophisticated models, actuaries can predict future payouts and set premiums that are competitive yet sufficient to cover potential claims.

Other Industries

Actuaries are equally vital in other industries. In the finance sector, an actuary might work for an investment firm, analyzing market trends and economic data to help manage investment risks. For instance, when an investment firm wants to introduce a new retirement savings product, the actuary evaluates various risk factors, such as market volatility and interest rate fluctuations, to design a product that maximizes returns while minimizing risks for investors.

In healthcare, actuaries play a key role in designing insurance plans that balance cost and coverage. A health insurer might hire an actuary to analyze data on treatment costs and health outcomes. The actuary’s analysis helps the insurer set premiums that are affordable for policyholders while ensuring the company can cover the cost of claims.

Practical Advice

For those considering a career as an actuary, gaining practical experience through internships and related roles can be invaluable. Engaging in real-world projects, such as risk assessments or financial modeling, provides hands-on experience that complements academic learning. Aspiring actuaries should also focus on developing strong analytical and problem-solving skills, as these are crucial for success in the field.

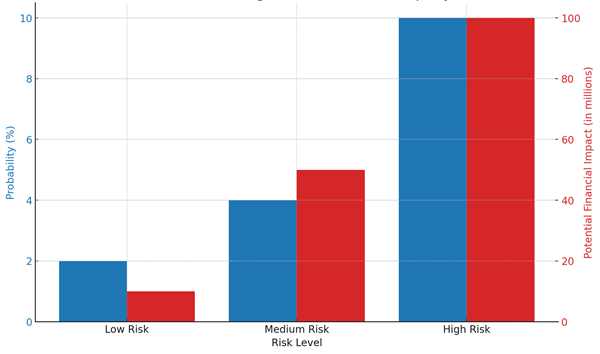

Risk Assessment Example: Evaluating Hurricane Risk for Property Insurance

The chart will show the probability of different levels of hurricane risk and their associated potential financial impacts.

The chart above illustrates the probability of different levels of hurricane risk and their associated potential financial impacts for property insurance.

Low Risk:

- Probability: 2% chance per year (1 in 50 years)

- Financial Impact: $10 million

Medium Risk:

- Probability: 4% chance per year (1 in 25 years)

- Financial Impact: $50 million

High Risk:

- Probability: 10% chance per year (1 in 10 years)

- Financial Impact: $100 million

Conclusion

Actuaries play a crucial role in assessing and managing risk across various industries, ensuring financial stability and effective risk management. Their work is essential not only in the insurance sector but also in finance, healthcare, and pensions. By understanding the skills, qualifications, and responsibilities of actuaries, as well as the differences between actuaries and underwriters, individuals can make informed decisions about pursuing a career in this field. The practical examples and visual aids provided throughout this page aim to demystify the actuary profession and highlight its importance in today’s complex financial landscape. Whether you’re considering a career as an actuary or simply seeking to understand the profession better, this comprehensive guide offers valuable insights and practical advice.

{kind=link}